Q1 2026 NCREIF US Farmland Value Regional Review; Regional Divergence Continues as Broader Row Crop Values Stabilize

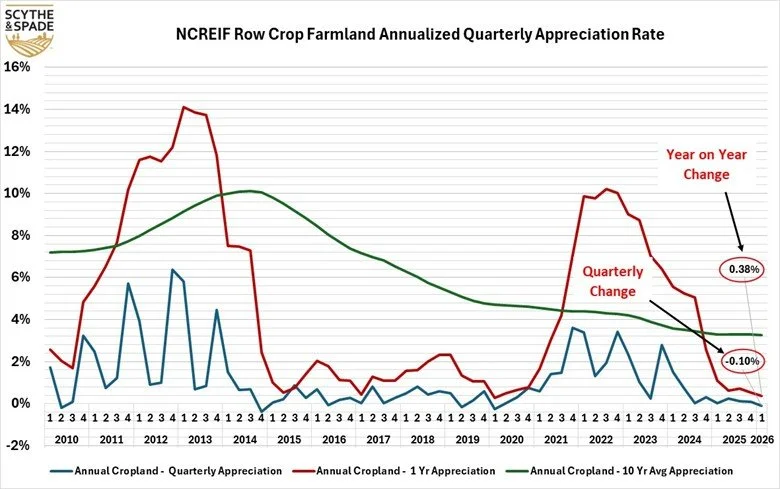

US row crop land values remained resilient in Q1 2026 despite continued regional fragmentation beneath the surface, posting a year-over-year increase of +0.38%. Although quarter-over-quarter values softened slightly at -0.10%, farmland as an asset class continues demonstrating its characteristic stability relative to other real assets. Regional performance increasingly reflects localized pressures tied to commodity economics, water availability, operating margins, and investor positioning.

Year-over-year Q1 2026US row crop land continued the long-running trend of avoiding annual portfolio-level value declines despite ongoing stress in agricultural operating conditions. Similar to prior periods, modest national gains masked increasingly wide dispersion between stronger and weaker producing regions.

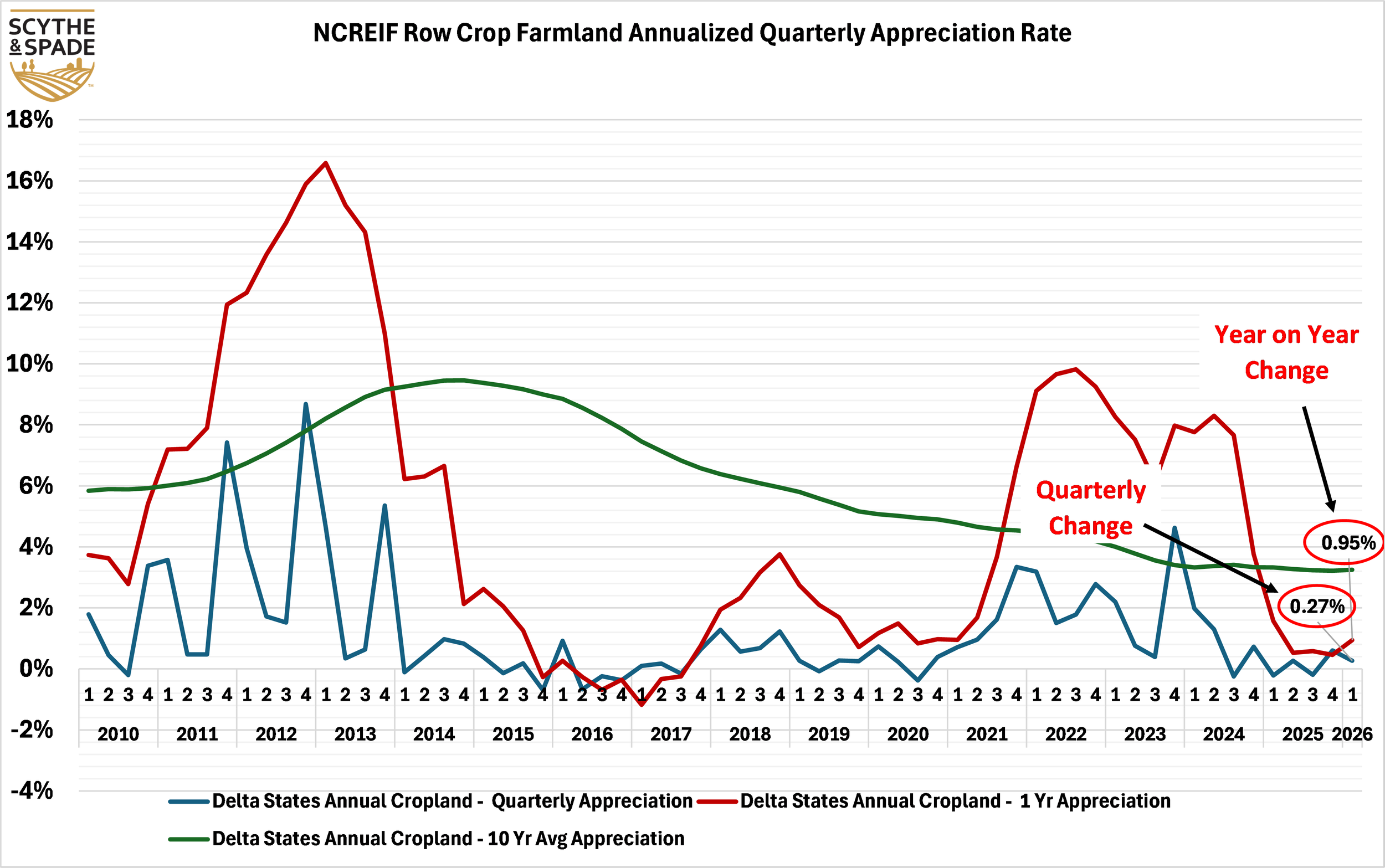

DELTA STATES

Delta row crop farmland remained one of the more stable performing regions within the NCREIF portfolio in Q1 2026, posting a year-over-year increase of +0.95% and a quarter-over-quarter increase of +0.27%. Values continued moving modestly upward, supported by relatively lower land basis levels, irrigation infrastructure advantages, and stronger relative cash rent stability versus higher-priced Midwestern regions.

The Delta continues benefiting from lower entry costs and a more favorable relationship between commodity returns and underlying land values. While producer margins remain compressed, valuation pressure has thus far been less severe than in regions where land values accelerated more aggressively during the 2021–2023 appreciation cycle.

Investor demand also appears comparatively durable in the region as buyers continue searching for productive acreage with lower absolute pricing and acceptable current yield characteristics.

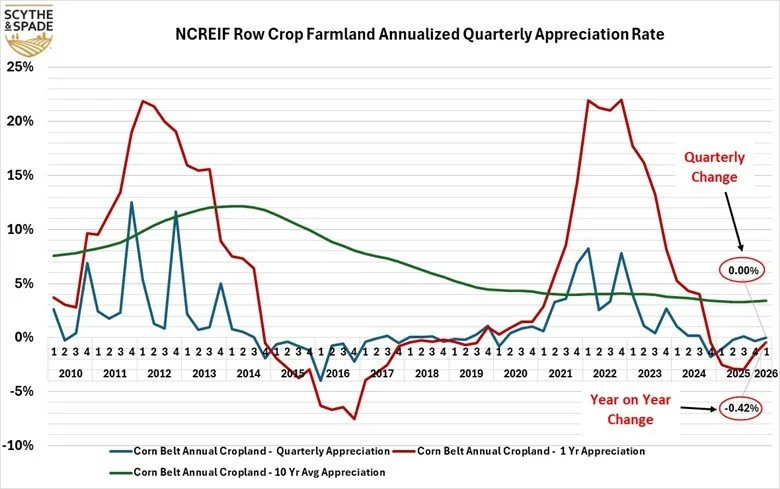

CORN BELT

Corn Belt farmland remained relatively flat in Q1 2026 with quarter-over-quarter returns of 0.00%, while posting a modest year over year decline of -0.42%. The region continues adjusting to a lower commodity price environment and tighter farm operating margins following the rapid appreciation cycle of 2021 and 2022.

The current correction increasingly appears tied to a normalization of capitalization assumptions after several years in which land values materially outpaced the underlying economics of row crop production. Elevated borrowing costs, weaker grain prices, and moderation in producer liquidity continue pressuring transaction activity and buyer enthusiasm.

That said, despite recent softness, Corn Belt land values remain substantially above pre-2021 levels. Long-term institutional conviction in the region remains intact given its productivity, infrastructure, and liquidity advantages, however investors are becoming materially more selective on soil quality, drainage, lease structures, and local basis dynamics.

PACIFIC NORTHWEST

Pacific Northwest row crop farmland remained among the stronger performing regions in Q1 2026 with a year-over-year increase of +2.33% and quarter-over-quarter appreciation of +0.13%. The region continues benefiting from crop diversity, export-oriented production systems, and comparatively constrained land supply.

However, similar to the prior quarter, the pace of appreciation continues to decline. While still positive for both year-over-year and quarter-over-quarter, returns appear increasingly reflective of stabilization rather than continued acceleration.

The Pacific Northwest remains one of the more differentiated farmland regions within institutional portfolios due to its unique crop mix and the lowest correlation with other regions. As a result, it continues attracting interest from investors seeking diversification within agricultural real assets

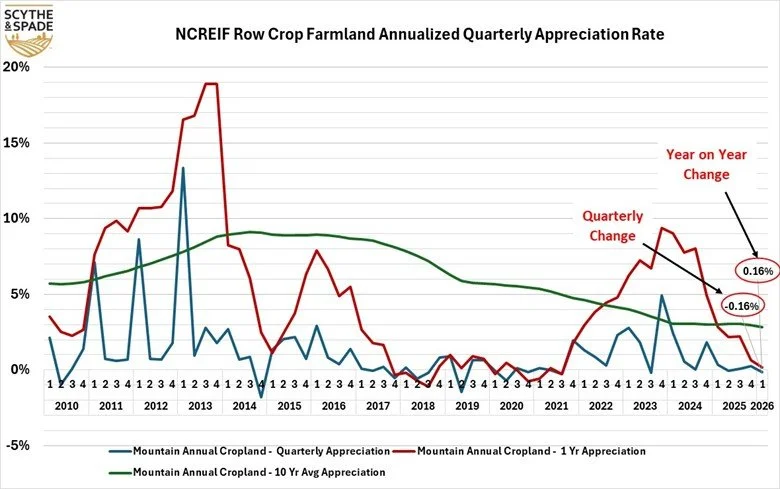

MOUNTAIN STATES

Mountain state row crop land values remained relatively stable in Q1 2026, posting a modest year-over-year increase of +0.16% despite a quarter-over-quarter decline of -0.16%.

The region continues lagging broader national farmland cycles by several quarters, consistent with prior periods. Lower transaction volume and thinner institutional participation can create slower valuation adjustments both during periods of appreciation and correction.

Operationally, the region continues facing many of the same pressures present nationally including elevated financing costs and weaker producer margins. However, relatively lower land values and localized supply constraints have thus far helped stabilize pricing.

CALIFORNIA ROW CROPLAND

California row crop farmland remained under significant pressure in Q1 2026 as water risk, operating costs, regulatory uncertainty, and investor caution continued weighing on values. NCREIF California row crop land values declined -4.76% quarter-over-quarter and -6.93% year over year.

The broader trend continues reflecting a prolonged repricing process tied primarily to water availability and long-term sustainability concerns. Increasingly, institutional focus is shifting away from simply identifying productive acreage toward determining which specific water profiles, groundwater positions, and regulatory exposures remain investable over long-term holding periods.

The market also continues differentiating sharply between individual assets rather than treating California farmland as a uniform category. Water district positioning, groundwater sustainability exposure, permanent versus annual crop flexibility, and recharge potential are all becoming increasingly central drivers of valuation.

Although the pace of decline remains significant, investors continue approaching the region cautiously amid uncertainty surrounding long-term water allocation and asset durability.

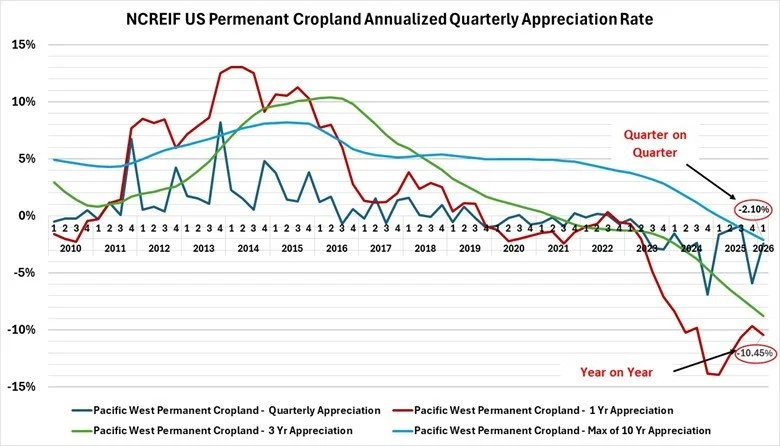

CALIFORNIA PERMANENT CROPLAND

California permanent cropland remained the weakest segment within the broader NCREIF farmland portfolio in Q1 2026, posting a quarter-over-quarter decline of -2.10% and a year-over-year decline of -10.45%.

An improved but still negative quarter-over-quarter return may reflect improved but uneven nut market conditions, with almonds still under margin pressure despite recent price recovery, while pistachio economics remain comparatively stronger. Unlike annual row crop acreage, permanent plantings possess limited operational flexibility once established, amplifying valuation sensitivity during downturns.

Importantly, the longer-duration rolling averages included in the chart continue illustrating the magnitude and persistence of the correction that began in late 2019. Multiple consecutive years of value decline have now pushed both the three and ten year rolling averages into negative territory.

Despite these pressures, market sentiment has improved modestly relative to the trough conditions observed during earlier phases of the downturn. Transaction activity appears slowly returning for select high-quality assets with secure water positioning, suggesting investors may increasingly believe the market is progressing through the later stages of repricing rather than the early stages.

SUMMARY

NCREIF farmland returns continue providing a more granular and institutionally relevant perspective on agricultural real estate trends than USDA data alone. While the broader US row crop portfolio has once again demonstrated resilience at the aggregate level, regional divergence continues widening beneath the surface.

The current environment increasingly rewards specialization, local operational knowledge, and careful underwriting rather than broad exposure alone. Water access, regulatory exposure, crop flexibility, and regional operating economics are becoming increasingly important determinants of long-term value stability.

Farmland continues maintaining many of the characteristics that have historically made it attractive to institutional investors, including inflation protection, low long-term correlation to traditional financial assets, and relatively durable underlying demand fundamentals. However, the sector is also becoming increasingly segmented between regions and asset types positioned for long-term resiliency and those facing more structural challenges.

As the current correction progresses, dislocations continue emerging across multiple farmland regions. For investors capable of underwriting operational, water, and geopolitical risks correctly, the present environment may continue creating selective opportunities to acquire quality agricultural assets at materially improved relative valuations.