Ranchland As an Investment

By: Sidnee Hill

After what could arguably be some of the toughest drought years in the south and a hellish calving season in the west, ranchers finally have a reason to smile. Record breaking calf and cull cow prices this year have far exceeded expectations.

For years US ranchland has taken a bit of backseat to the more prevalent farmland, even being seen by many as more of a “lifestyle” investment. But does this year’s near record breaking cattle prices signal a permanent change in Industry returns? Should we be looking at ranchland investments with fresh eyes? While things feel unpredictable, the cattle industry is still following basic economic principles that can help guide our investment making decisions. There are, however, some unique economic features about the beef industry that we must first understand.

A Multi-Step Supply Chain:

The US beef supply chain is a complex behemoth, that has many steps along the way to the consumer (figure below). Each step along this chain operates almost independently with unique market factors. A boon in one step of the chain does not necessitate profits throughout the entire stream. For example, Greg Henderson’s Drovers article titled Profit Tracker: Feeding, Packing Margins Remain Red, shows that while calf producers continue to enjoy historically strong prices, cattle feeders and packers are operating on negative margins of -$10 and -$38/head respectively in November[1] 2023. When investing in ranchland it is important to understand which parts of the beef supply chain you are investing in and how that will impact your expected returns. The prices and data that we will be referring to in this article will relate to commercial cow-calf production.

Beef Supply

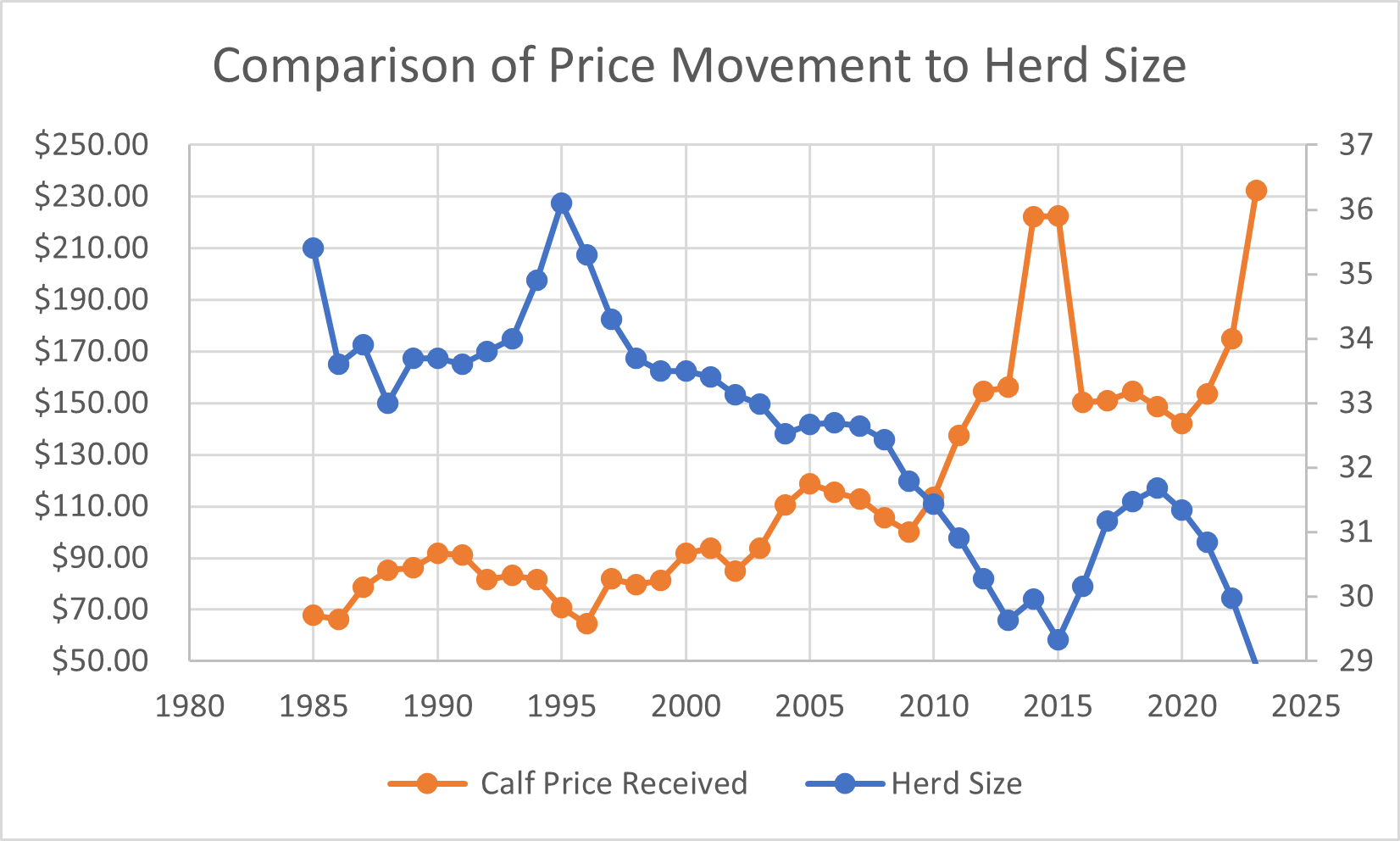

As true in your college Econ 101 as it is today: price is determined by the independent factors of supply and demand. For now, we will put aside demand until our next article and focus on supply. Supply in the beef industry is affected by the following: weather, cost of inputs, regulation, grower expectations, and available capital. Since 2011, farm input prices have increased by 38.8%. Feed price alone, which is the largest expense in ranching, has increased by 26% in that same period. Throw in the stew pot record nationwide drought, killer snowstorms, and limited and expensive capital to invest in breeding stock- it is no wonder we come out with the smallest national beef herd size since 1962 (figure below). This contraction is important in two ways: 1. As the herd size decreases (and beef demand remains stable) prices received for calves increases, and, 2. herd size fluctuations are fairly predictable through the cattle cycle.

The Cattle Cycle:

As mentioned, national herd sizes follow an uncanny cycle of predictability, a peak-trough-peak cycle that regularly happens every 8-12 years. And where herd size goes, cattle prices will move in the opposite direction.

Our quick calculations show a correlation factor of -0.734 over the last eight years between prices received for calves and national herd size. (Remember the closer a correlation factor is to 1 the more perfectly they move together.) Today, after an 8-year contraction, we find ourselves at or near our next price peak. To know where prices are heading from here, following herd size will give us a strong indication. Our big question is now very simple: is the national herd size rebuilding? A rebuilding herd would signal a future leveling or decline in prices.

The big red flags that signal herd expansion in the US are a decrease in cow slaughter and an increase of retained heifer numbers. We started 2023 with the lowest level of replacement heifers and springers (heifers expected to calve) since 2011[2]. Since then, the reported number of heifers on feed (for slaughter instead of replacements) has increased 1.3% since last October 2023[2]. In short, it looks like producers are not retaining as many heifers as will be needed to start a significant herd rebuild. Barring war, crazy politicians, black swans, or grey rhinos; we can optimistically expect cattle prices to remain comparatively higher into next year.

As an investor this has implications for not only how much you will have to pay for your cattle assets, but how analyst may be determining the valuation of your ranchland investment as well. Since we are at or nearing a price peak, we can comfortably assume that over the next 3-5 years calf prices will once again be tracking down. A careless analysis that doesn’t take into consideration these price movements and only includes our current, high prices will surely spit out a skewed result.

Calculating Fair Rent:

Future revenue streams from rent is another key consideration when exploring ranchland as an investment. While there is a myriad of leasing options, ranchland income can be generated from two general categories: 1. Own just the land and lease pasture out for grazing, or, 2. Own the land and the cattle and reap the returns from calf sales. Both come with their own balance of risk and reward that should be carefully considered.

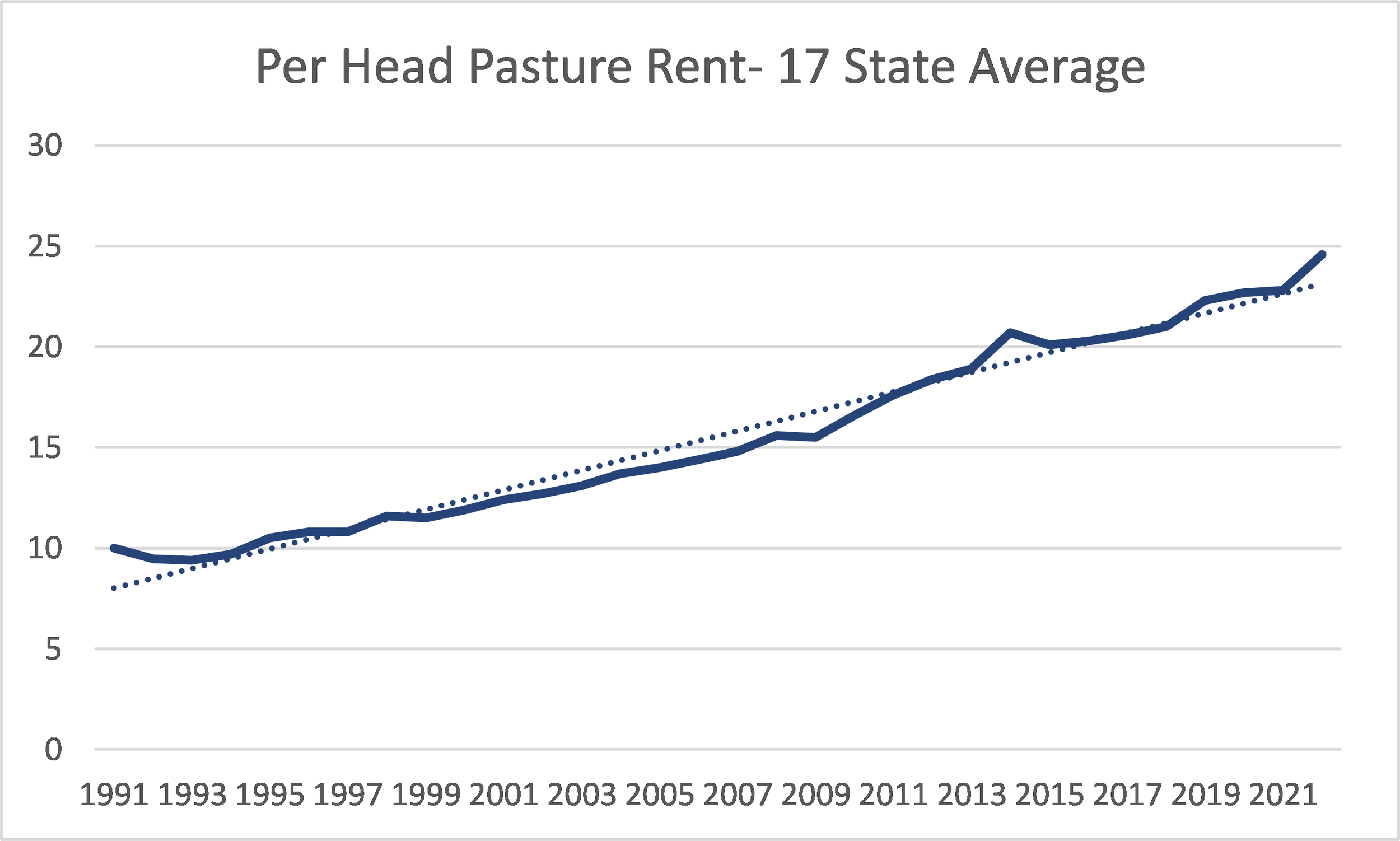

In either situation, per-head pasture rent from the USDA-NASS shows a steady upward march that increases about $0.48 a year since 1991. I highly recommend a thorough investigation into local pasture rent rates as they are highly variable across the country and subject to local market factors. But be warned: the credibility, experience, and oversight of whomever leases your grass cannot be overstated. Look to our next article for more information about this topic. When establishing a fair lease rent, take care to once again utilize a 7-10 year rolling average (to capture latest peak and trough) of cattle prices. Anything shorter or longer in duration may give you unrealistic or unattainable representation.

The credibility, experience, and oversight of whomever leases your grass cannot be overstated Look to our next article for more information about this topic.

Should I Invest in Ranchland?

When deciding if you should invest in ranchland we must take a hard look at industry timing, your investment timeline, and your asset management plans. Are we at a price peak or a trough? When in a peak (such as what we currently find ourselves in) it may be worth considering ranchland as a short term (1-2 year) or long term (10 year) investments in order to capture those peak price windfalls and offset any mid-term decline. When investing during a price trough, or with a pasture leasing arrangement only, plan for mid length holdings (5 year) and/or lifetime investments.

However, as with all agricultural land, the devil is in the details. Many factors including environmental, regulatory, and scale will factor into the suitability of a ranch for investment. If you are considering adding ranchland to your portfolio, don’t go it alone! Through the whole process of identifying, purchasing, and managing your ranch consider utilizing the 100+ years of expertise and ranch management experience we hold here on the Scythe and Spade team[BM1] [SH2] [MH3]

[1] Profit Tracker: Feeding, Packing Margins Remain Red | Drovers

[2] Cow and Heifer Slaughter Indicates Continued Herd Liquidation | Drovers